A greener footprint

The food and beverage sectors dominate the usage of labels worldwide, with the leading global supermarket groups and major brands having a significant influence on packaging and label purchasing trends.

This dominance has meant that supermarkets have built-up an almost unprecedented economic, purchasing and political power in the food and beverage sector, as well as a having a growing responsibility in promoting and demonstrating a high degree of corporate social responsibility.

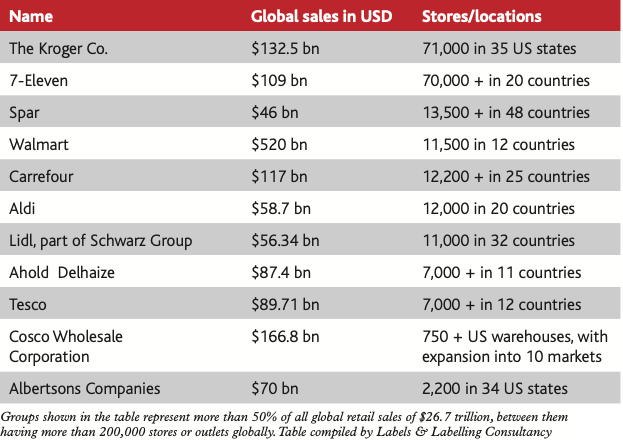

One recent report highlighted that a third of global food sales were made by the world's ten largest supermarket chains. Another study found that food and beverage applications together accounted for about 30 percent of all global label demand, while the supermarket groups identified by Labels & Labelling Consultancy in the highlighted table – with more than 200,000 stores or retail outlets between them ̶ are believed to represent more than half of global retail sales in a market estimated to be in excess of 26 trillion USD. That's a lot of labels that require printing annually.

Another recent study points out that by 2027 the food and beverage end-use sectors are expected to hold more than 55 percent of the global label market share. One important consequence of such supermarket domination, especially in the food sector, has been the steady and continuous growth in supermarket own-brand foods (also identified as private label, in-house brand, store brand, retailer brand or home brand), which are actually owned by the supermarket retailer, wholesaler or distributor and are exclusively sold in their own retail outlets.

Consequently, the leading supermarket groups have a key role in not only selling the products but also in their manufacture ̶ including the detailed specification of the packaging and labels, the sourcing of packaging and label materials, and the supermarket and supplier relationship. In certain areas the supermarket groups have even come together with a common aim. As an example, 31 of the world's largest supermarkets have committed to taking steps to improve sustainable sourcing of raw materials.

Reduce, reuse, recycle, renew

Many of the leading supermarket groups assess their packaging and labels against the 4R Guidelines (Reduce, Reuse, Recycle, Renew), both working to reduce packaging and increase the recyclability of their packaging (and label) materials. A key aim is to make packaging recycling easier for customers. Carrefour, for example, aims for 100 percent recyclable, reusable or compostable packaging for its own brands by 2025.

A further company focusing on a 4R strategy is Tesco, a near 90 billion USD supermarket chain with around 7,000 stores in 12 countries. has been prioritizing ongoing removal of unnecessary packaging and working with suppliers and partners to reduce, reuse and recycle packaging. Its commitments include the removal of plastic packaging where it can, and introducing a scalable reusable packaging offer for customers.

Other leading supermarket groups have become signatories of the Ellen MacArthur Foundation's New Plastics Economy Global Commitment in which they are working towards zero plastic waste from their own-brand packaging by a specific target date and by making the plastic packaging they use 100 percent recyclable, compostable or reusable. Some of the groups have developed a holistic internationally applied strategy that comprises five action areas: from avoidance and design to recycling and removal, up to innovation and education, with a vision of ‘less plastic – closed loops’ becoming a reality.

Many of the supermarket groups, such as Lidl with some 11,000 stores in 32 countries, have also set ambitious carbon reduction targets and are looking to work collaboratively with their suppliers to establish their own climate targets and strategic plans for the next five years or more. Aldi too, with stores in 20 countries, has stated that it is continually working to reduce the amount of plastic and packaging that it uses, and to ensure that the materials it does use are easy for customers to recycle.

As the world's largest retailer in terms of sales, with over 500 billion USD in revenue annually, Walmart is working with US private brand label and packaging suppliers to achieve 100 recyclable, reusable or industrially compostable packaging for its private brand packaging by 2025. It is also targeting at least 20 percent post-consumer recycled content in private brand packaging by 2025.

With the focus of the circular economy on reducing, reusing and recycling, Spar’s drive to redesign packaging has gained increased importance. Indeed, across Spar's 13,500 stores in some 48 countries, its partners are working to ensure unnecessary packaging and non-recyclable materials are removed from Spar own-brand products wherever possible. Key considerations are to ensure reduced CO2 emissions at the production phase and reduced energy consumption during recycling processes.

In the Netherlands, Dutch grocery retail company Ahold Delhaize has a family of local brands that serve more than 54 million shoppers each week in 11 countries. It is working towards zero plastic waste from own-brand packaging by 2025 by making the plastic packaging it uses 100 percent recyclable, compostable or reusable, and aims to minimize the overall lifecycle impact of its products through packaging optimization.

Also looking for ways to improve packaging by using eco-friendly materials, reducing content and decreasing the use of plastic whenever possible is 7-Eleven, with an estimated 70,000 outlets in 16 countries, and global sales in excess of 100 billion USD. With much of its eco-friendly packaging including renewable or recycled content, or derived from sustainable resources, it is working to reduce packaging materials wherever possible.

In the USA, Kroger Co. with a family of around 71,000 stores ̶ including brands such as Baker's, City Market, Dillons, Fred Meyer, Jay C Food Store, Pay-Less, Ralphs ̶ and covering some 35 US states, is claimed to be the world's largest supermarket chain. It has been piloting reusable packaging systems, enabling consumers to purchase more than 100 products that have been redesigned with durable containers.

Also in the USA is Costco Wholesale, an American multinational which operates a chain of membership-only big-box retail warehouse stores. As of 2020, it was rated the fifth largest retailer in the world, and the world's largest retailer of prime beef, organic foods, rotisserie chicken and wine. Costco continues to look for ways to improve the design of its packaging to reduce the amount, improve the efficiency, and improve operational efficiencies in order to reduce the packaging footprint and reduce costs. Its goal is for all packaging to be widely recyclable and/or made from recycled content.

Commitment

Go beyond the top ten or so global supermarket groups discussed above to look at the top 50 or even the top 100, and pretty well all of them are committed in various way to improving their packaging and label footprint over the next five or six years. This commitment obviously has implications for all the packaging and label producers looking to serve the food, supermarket and beverage sectors.

If these commitments already seem to be quite stringent then the packaging and label producer needs to realize that the current supermarket policies were all drawn-up before the recent 2021 IPCC Report on global warming and the October COP26 Climate Conference in Glasgow took place, both of which will likely end-up putting further pressure on the global supermarkets and brands in terms of sustainable development and low carbon goals and, in turn, on label and packaging producers.

Much has changed over the past 18 months: the global pandemic has created many challenges for physical store retailers. The global market share of big supermarkets is now shrinking as a growing order of discounters and e-commerce continues to take hold. Amazon, for example, with global retail sales in excess of 380 billion USD in 2020, is the largest publicly traded market capitalization, while Alibaba (sales revenue 120 billion USD) is a world champion in sales via marketplace platforms.

As a consequence, many global supermarket groups have been facing pressure to reduce costs, rationalize product ranges, provide more own-brand products, and to develop or expand their own online shopping offerings. All of these factors have implications for label and packaging groups.

While the supermarket groups are the world's largest grocery and food retailers and undoubtedly have a major influence on label and package sourcing, especially of their own-brand products, similar patterns of influence are found in many other label end-user sectors. Just 10 companies for example, are said to be involved in or control pretty well almost every major food and beverage brand found and sold on grocery shelves worldwide: Kraft Heinz Company, PepsiCo, Nestlé, P&G, Unilever, Johnson & Johnson, Kellogg's, Coca-Cola, General Mills and Mars.

Take any one of them to look at in more detail. Nestlé is a partner of the Ellen MacArthur Foundation's New Plastics Economy initiative, and has announced its ambition to make 100 percent of its packaging recyclable or re-usable by 2025. Its vision is that none of its packaging, including plastics, ends up in landfill or as litter. All the other food and beverage brands have similar kinds of packaging footprint programs.

The same can be said of the world's biggest pharmaceutical companies ̶ such as Pfizer, Roche, Bayer, Novartis, Merck & Co, Johnson & Johnson, Sanofi SA, Bristol-Myers Squibb, GlaxoSmithKline and AstraZeneca ̶ all of which have annual sales revenues of between around 40 billion and 80 billion USD. Again, as an example, Pfizer is dedicated to collaborating across its supply chain to reduce the environmental footprint of its packaging throughout its lifecycle.

Put all of this research together and the conclusion is that probably less than a 100 or so global super groups are responsible for specifying, sourcing, designing and buying the great majority of all the world's labels and packaging, and for driving forward sustainable packaging programs, circular economies, packaging compliance, and carbon reduction initiatives. The recent 2021 IPCC Report on global warming and the October COP26 Climate Conference in Glasgow are likely to put further pressure on these groups to bring forward and enhance such initiatives.

Put all of this research together and the conclusion is that probably less than a 100 or so global super groups are responsible for specifying, sourcing, designing and buying the great majority of all the world's labels and packaging, and for driving forward sustainable packaging programs, circular economies, packaging compliance, and carbon reduction initiatives. The recent 2021 IPCC Report on global warming and the October COP26 Climate Conference in Glasgow are likely to put further pressure on these groups to bring forward and enhance such initiatives.

Such pressures are undoubtedly going to also be pushed down the supply chain to the label and packaging suppliers in terms of materials sourcing, minimizing the use of plastics, cost reduction, carbon reduction, sustainability and recycling. If the label and packaging converter wants to understand where their major buying customers are going to take them over the five or ten years, then a study of their packaging footprint policies would be a good start.

Stay up to date

Subscribe to the free Label News newsletter and receive the latest content every week. We'll never share your email address.